Tougher times ahead as the mining boom shifts gears

Tuesday, Feb 5, 2013, 07:51 PM | Source: The Conversation

Ian Harper

Various explanations have been offered for Prime Minister Julia Gillard’s decision to announce the date of the 2013 federal election almost eight months in advance. Most commentators, both those who applaud the move and those who decry it, focus on political tactics, but economics should not be overlooked.

The Australian economy is shifting gears. The Reserve Bank’s index of commodity prices has fallen 20% from its peak in 2011, pulling down Australia’s terms of trade (ratio of export prices to import prices). Falling export prices, other things equal, slow the growth of national income even as national output continues to grow at more or less the same pace. The point is simply that our customers pay less for what we sell them even though we sell the same volumes, resulting in lower export revenue or income to us.

Slower growth of national income will make for tougher economic times. For a start, the chances of the government balancing the federal budget have all but disappeared, at least without quite marked (and electorally risky) reductions in federal outlays. Falling national income hits budget revenue, both at the state and Commonwealth levels, forcing expenditure restraint onto deficit-conscious governments.

Falling national income has had a similar dampening effect on the revenues of private firms, leading them to shelve planned investment and labour-hiring plans. Consumers see all of this and become even more cautious, moderating their consumption and increasing savings.

This dampening influence will continue as long as export prices keep falling — or until something else turns up. In fact, something is expected to turn up, but not until the second half of 2013―hence the contribution of economics to the PM’s choice of polling date.

While no-one is predicting a turnaround in Australia’s export prices anytime soon, export volumes are set to pick up as the mining boom morphs from its investment phase into its export phase. Many commentators, including the Reserve Bank, have predicted that mining investment will peak this year. Other things equal, falling levels of mining investment will add further negative impetus to income growth notwithstanding the near-stratospheric levels that mining investment has reached as a share of gross domestic product during this boom.

But other things are not equal. As mining investment begins to wane, mining exports begin to wax. Export volumes will rise as mining projects come on line, most especially in oil and gas. Importantly, export volumes are expected to contribute positively to economic growth well into the foreseeable future.

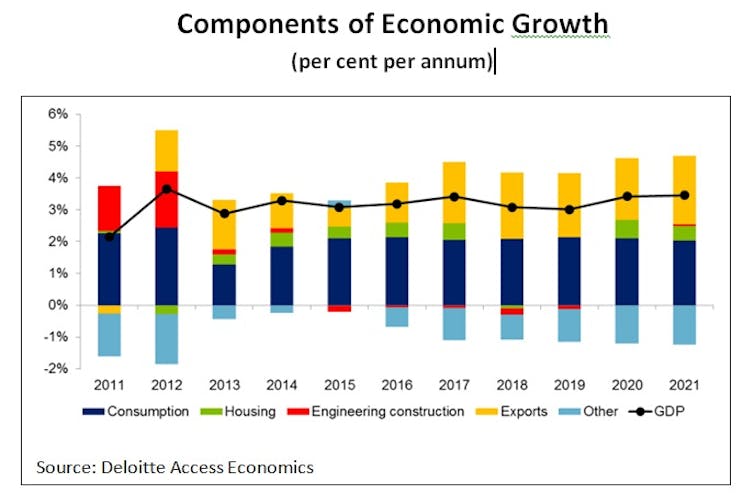

The accompanying chart illustrates the economic gear-shift that Australia is currently negotiating. Engineering construction — the on-the-ground manifestation of mining investment — is forecast to contribute substantially less to GDP growth in 2013 than it has since the onset of the boom. However, as mining investment tails off, mining exports are expected to pick up; indeed, the composition of GDP growth reflects an ongoing contribution from exports to the end of this decade and beyond.

Looking at the chart, we see that the changeover is not entirely smooth. Aggregate economic growth is expected to slow during the transition because mining export growth will pick up more slowly than mining construction tails off. This is likely to be more evident in the first half of 2013, when we can expect to see some uptick in the rate of unemployment and at least one further cash rate reduction from the Reserve Bank to prevent too much clashing of the gears on the way through.

The gist of the so-called “political business cycle” theory is that governments win or lose elections according to economic conditions prevailing at the time. Delaying the federal election until the second half of 2013 makes sense if the forecasts are right and the government can point to improving conditions.

The transition from investment-led to export-led growth should also modulate upward pressure on the exchange rate for the Australian dollar. Foreign capital inflow has funded much of Australia’s mining investment boom and the sharp run-up in this boom has taken the exchange rate with it. Export-led growth will still sustain the exchange rate above what most economists acknowledge as its longer-run value (something well below parity with the US dollar) but should allow some room for depreciation from recent highs.

The high exchange rate for the Australian dollar is the mainspring of the “two-speed” economy and its attendant economic and political tensions. Whichever party assumes government following the September election, the fallout from such an extended period of exchange rate appreciation on those non-mining parts of the economy exposed to foreign competition will still be evident.

The challenge for both political parties is to help Australians understand the economic transition we are experiencing and to look to the longer-term benefits for Australian living standards and prosperity.

Ian Harper does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.