Carbon tax a step towards reform, but working mothers miss out

Monday, Jul 11, 2011, 01:13 AM | Source: The Conversation

Miranda Stewart

At first glance, the Federal Government’s carbon tax plan appears to carry out significant income tax rate reform in the guise of carbon price compensation.

Indeed, the proposed tax rate reforms adopt the essence of recommendations by the 2009 Henry Tax Review of Australia’s Future Tax System.

But it is worth delving into the detail to fully understand how some will benefit more than others - and perhaps not the ones we think.

Treasury modelling for the Federal Government’s carbon plan estimates the cost-of-living impact of its $23 per tonne carbon price will increase inflation by 0.7%, as measured by the consumer price index for 2012-13.

To compensate for this increase in the household cost of living, the government claims that “every cent raised from a price on carbon will be used to provide tax cuts and increased benefits to households, support jobs in the most affected industries, and build a new clean energy future.”

As a result of its income tax cuts, higher Family Tax Benefits, and increases in pensions, allowances and other benefits, it argues that “around two out of three households will receive assistance that offsets their average cost of living impact. Many households will be better off.”

Everyone will be affected

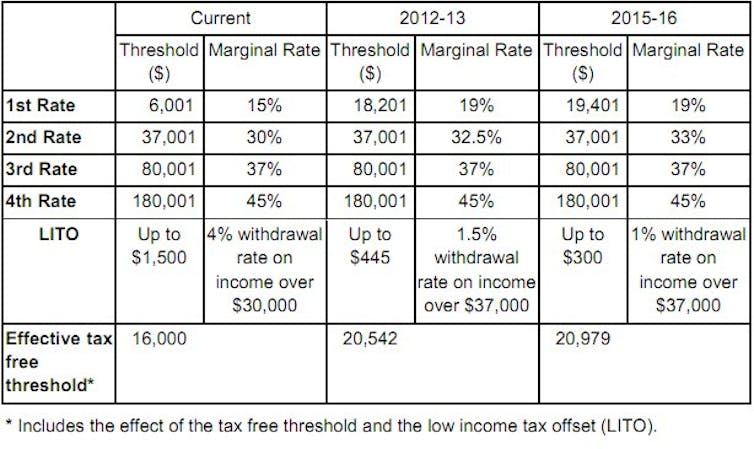

The proposed changes are focused on the tax-free threshold and lowest two rates of tax, but will affect all taxpayers because even those facing the top marginal rate are affected by the bottom two rates.

The changes are illustrated in the following table, taken from the Clean Energy Future plan.

The biggest change is a threefold increase in the tax-free threshold to $18,200 in 2012 and $19,400 in 2015. Australia has had a tax-free threshold of $6,000 (and before that, $5000) for decades.

Tax on the lowest income earners is currently eliminated by the low income tax offset (LITO), which now stands at $1500 and phases out at 4 cents in the dollar from $30,000.

The plan leaves a small LITO remaining, which phases out at 1.5 cents in the dollar over approximately the same range. This is illustrated in the table below.

From low to high incomes, the impact explained

Assume Ann has taxable income of $27,000 (from part-time work); Ben has taxable income of $67,000 (reflecting average adult full time weekly earnings) and Charles has taxable income of $200,000 (the government defines “high income” as $150,000 in the proposal).

Currently, Ann pays $1650 of income tax plus the Medicare Levy of $405, a total of $2055; she benefits from the zero tax threshold and 15% marginal rate, plus the full Low Income Tax Offset of $1500. She has an effective average tax rate of 7.6%.

Under the carbon price plan, Ann pays a total of $1728 in tax, including the Medicare Levy. She benefits from the tax-free threshold and from the reduced LITO. Her effective tax rate is reduced to 6.4%.

Earning average weekly earnings, Ben pays income tax of (6000 * 0%) + [(37000-6000) * 15%] + [(67,000 – 37000) * 30%] + Medicare Levy of 1.5% ($1,000) = $14,650. He faces a marginal tax rate of 31.5% and an effective tax rate of about 21.9%.

The carbon price compensation would ensure that Ben pays no tax on the first $18,200 of income but pays higher rates of 19% on income up to $37,000 and 32.5% on his remaining income. Ben’s total tax bill will be $14,322, a saving of $328 a year and a reduction in effective tax rate of 0.6%, down to 21.4%.

Currently, Charles pays income tax of $63,460 + Medicare Levy of 1.5% (3,000), a total of $66,460. Charles faces a marginal tax rate of 46.5% and an effective tax rate of 33.2%.

After carbon price compensation, Charles total tax bill will be almost identical, at $66,547. Although the plan states that no person will pay more income tax, it appears that there may be a small increase in tax for Charles of $87 per year. For most high income earners, however, their tax position is essentially unchanged by the package, so that they will bear the full cost of the carbon price impact.

This should mean that they face the maximum incentive to reallocate their household expenses towards low polluting products.

As always, kids make it more complicated

For taxpayers with dependent children, the compensation package will increase Family Tax Benefits A and B by 1.7%, to be paid as a lump sum for the first year. These Family Tax Benefits, like many other benefits (such as the age pension), are means-tested on couple income. However, delivering assistance on this basis can generate different outcomes for individuals within the household.

Assume Ann and Ben are spouses and they have two young children.

If Ann does not earn a salary, Ben will be able to claim Family Tax Benefit A and Ann can claim Family Tax Benefit B. Combined, this will generate additional income for them of about $10,000 (increased to compensate for the carbon price). This reduces the effective tax rate faced by Ben, based on his taxable income of $67,000 (and hence on the household as a whole) to about 8%. In reality, it is even lower, as the benefits of ‘home production’ of childcare and other household services by Ann are not taxed.

Now consider the impact if Ann goes back to work three days a week and earns $27,000. Ben is entitled to the base rate of Family Tax Benefit Part A, about $4,200 for two children, but Ann is no longer eligible for Family Tax Benefit B.

Ann faces long-day childcare costs for three days/week (which could be $6/hour, or higher), for which she will be entitled to childcare benefits of about $12,000 which may, just, compensate for this childcare cost.

As explained above, on taxable income of $27,000, Ann currently pays tax of $2,055. However, the implicit effective tax rate faced by Ann is much higher because of phase out of Family Tax Benefit A as soon as she starts earning, initially at 20 cents, and as her salary increases, at 30 cents, for every dollar she earns. Her effective tax rate is almost as high as Charles, on $200,000.

After carbon price compensation, Ann pays a bit less tax, but the compensation package leaves the phase out rates of Family Tax Benefit unchanged.

Mothers miss out on real reform

The government states that to ensure that single income families are properly compensated, an additional supplement may apply for those families which “benefit less” from income tax reform than dual income families. But this compensation package fails to remedy the fundamental tax rate bias against mothers who return to work and earn low to middle incomes, in dual income families.

The carbon tax plan gives a nod to “secondary earners” such as Ann. It suggests that Ann will benefit from a more “transparent” system in which the low income tax offset is incorporated into the tax rate structure.

But it is clear that Ann will face the same high average and effective tax rates under the carbon price plan as she does under the current tax system.

If the government’s modelling of the carbon price impact stands up, the proposed tax and benefit changes appear to provide adequate compensation, on the whole. But in spite of appearances, this is not real tax reform.

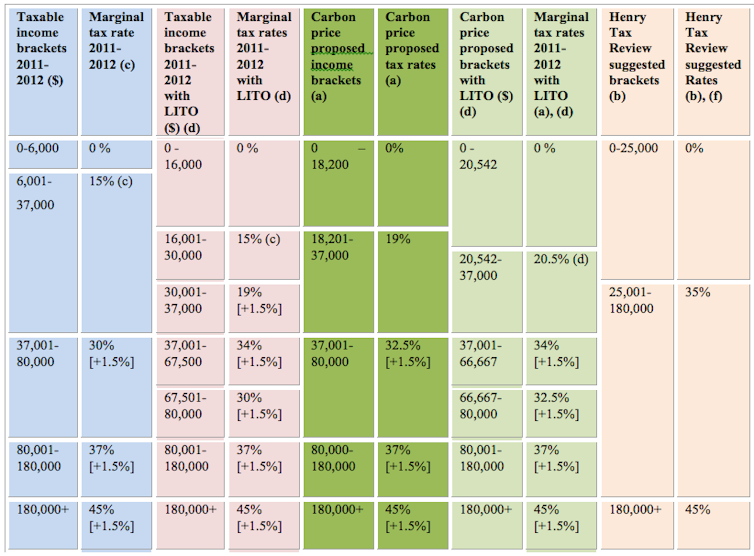

The minimal effects of the tax rate compensation are illustrated in the table below, which compares the current rate structure with and without the LITO, to the carbon price compensation package and the Henry Tax Review suggested rates.

Perhaps the government is leaving the real tax reform debate for the Tax Summit, scheduled for early October. But the rhetoric in the carbon price plan suggests that the government thinks that this plan achieves reform - and there is no money left in the carbon package for real reform that would reduce our high tax rates on mothers going back to work.

- For current tax rates see http://www.ato.gov.au

- Carbon price compensation package, announced 10 July 2011, http://www.cleanenergyfuture.gov.au/clean-energy-future/securing-a-clean-energy-future

- Henry Tax Review, Final Report, Treasury 2009: Part 1 29-30 and Recommendations 2 and 4, http://www.taxreview.treasury.gov.au

- For 2011-2012, the maximum low income tax offset is $1500 and it is phased out at 4 cents in the dollar between $30,000 and $67,500. The offset raises the zero threshold to $16,000. The carbon price plan reduces the LITO to $445, phased out at 1.5 cents in the dollar between $37,000 and $66,667.

- The Medicare Levy of 1.5% is levied on taxable income, phased-in within a narrow range for individuals ($18,839 to $22,164) and couples ($31,789 up to about $57,000 depending on the number of children).

- The Henry Tax Review recommends that the Medicare Levy be “rolled into” the personal tax rate structure (Recommendation 5). It is not clear whether the Review intends that this will have the effect of reducing marginal rates by 1.5%, with the particular effect of reducing the top marginal rate from 46.5% to 45%; however this is implicit in its recommendation.

Miranda Stewart receives funding from the ARC.