The $100 billion question: can Australia afford our retirement bill as the 'grey vote' booms?

Sunday, May 17, 2015, 08:09 PM | Source: The Conversation

Peter Gahan

Reining in the rising costs of an ageing population is politically perilous, as successive federal governments have discovered – and it’s about to get even harder as the proportion of older voters rises.

As the latest budget shows, the age pension is Australia’s single biggest welfare payment. It costs $44 billion in 2015-16 and will grow to $50 billion by 2018-19 - or about 10% of total federal budget spending.

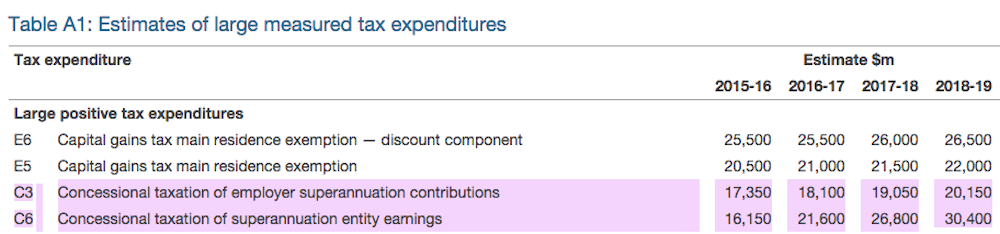

But superannuation tax concessions – which benefit wealthier retirees more than others – are fast catching up.

The latest budget shows that forgone revenue from two superannuation tax concessions will cost the federal government $36 billion this coming financial year, jumping to $50 billion in 2018-19.

Within three years, Australians will face a $100 billion-plus bill, just to cover the age pension and super tax breaks. Without action, that bill will be much higher as more baby boomers head to retirement.

By 2025, the Australian Bureau of Statistics estimates that one in three Australians will be aged 55 years or older, staying at around that level beyond 2050.

That’s significantly higher than today. Currently, around one-quarter of the population is 55 or older; almost half of this group is aged 55 to 64. Many people in this age group have retired, while the rest are in the final years of their working life and preparing for retirement.

Older workers and retirees are quickly becoming Australia’s most significant age group of voters – and will remain so for many years to come. As such, they will be crucial in shaping the choices future governments make on the road back to budget balance.

Pension promises and wavering support

After a political backlash against last year’s proposed pension cuts, this year the government is instead promising “a fairer pension system”, with more targeted changes starting in 2017.

Since Tuesday’s budget, Prime Minister Tony Abbott has gone even further to reassure retirees and older workers about superannuation, declaring:

There will be no changes to super, no adverse changes to super in this term of parliament, and we have no plans to make adverse changes to super in the future.

But that promise now risks seeing the $2.4 billion pension reforms being blocked in the Senate.

The latest budget confirmed that plans to index pensions at a lower rate have been dropped. The more stringent eligibility rules announced last year have also been abandoned in favour of an assets test, which will have more limited impact on most part-pensioners.

Couples who do not own their home will face a cut to their pension once the value of their assets rises above $800,000 ($500,000 for pensioner couples who own their home), falling to zero once their assets hit a little over $1 million ($823,000 for a pensioner couple who own their home).

Single pensioners will lose their pension once the value of the assets hits between $1 million (for non-homeowners) and around $550,000 (for homeowners).

But around 400,000 pensioners will actually enjoy an increase in their pension thanks to this budget.

Those pension proposals initially received in-principle support from key retiree representative groups. But some of that support appears to have evaporated since the details were announced in Tuesday’s budget.

Council of the Ageing chief executive Ian Yates has indicated that his group’s backing for pension reforms was conditional on the government also addressing super reforms. Criticising “piecemeal tinkering in some areas and neglect in others”, Yates has called for a broad, independent review of retirement incomes that includes not just pensions but also superannuation.

After the government ruled out such a review, Yates told The Australian Financial Review:

Our advice to the [Senate] cross benches is ‘don’t agree to the pension changes without the government committing to a retirement incomes review’.

(Not so) super reform

While significant numbers of retirees will continue to rely on the age pension, the proportion of all retirees who do so is set to decline, as the generation of Australians who have benefited from compulsory superannuation (introduced in the mid-1990s) head into retirement.

These will be the tail-end of the baby boomers and the Gen-X cohort. While this will signal budget relief in the future, this will not be so in this term – or the next – of a federal government.

The benefit of our compulsory superannuation system will not be fully reflected in the budget until around 2045: about the same time the trend towards an ageing of the population begins to reverse.

In the meantime, superannuation tax breaks are burning a growing hole in the budget. As last year’s inquiry into Australia’s financial system showed, the problem of superannuation is much larger than the current drain on taxation revenues. Current arrangements are poorly targeted and favour those who already have the largest superannuation balances.

Looking more broadly, the rules relating to when individuals can access superannuation are out of sync with pension eligibility rules. That creates an incentive for workers between the age of 55 and 60 to leave paid employment early – all at a time when government is promising to spend more in the form of a $10,000 employment subsidy to encourage employers to retain older workers.

Bipartisan failure

Reforming superannuation will be as politically difficult as pension reform has proven to be. It will inevitably create more losers than winners.

Little wonder the prime minister has ruled out any changes to super.

So what would a Labor government do?

Opposition Leader Bill Shorten has already made clear that a Labor government under his leadership would reform tax concessions applying to superannuation, but would do little to address the burgeoning cost of current pension arrangements.

That means the Abbott-led Coalition government only wants to tackle pensions, while Shorten’s Labor opposition only wants to tackle superannuation concessions.

So far, neither has signalled they are prepared to reform both the age pension and super tax breaks – the politically difficult but economically necessary task ahead.

Looking at the future more optimistically, Shorten signalled in his budget reply speech a willingness to take a more bipartisan approach to reduce the budget deficit and promote growth. Hopefully, this commitment extends to a review of retirement incomes.

Baby boomers were lucky, but still need retirement help

Right now, ageing workers are the core of the baby boomer generation. It is easy to caricature them as a lucky generation: born in the post-war period, they enjoyed an enviable period of extended economic prosperity and social freedom.

The baby boomers formed families and bought houses at a time when housing was relatively cheap and affordable. Their kids enjoyed free university education. They now benefit from the significant wealth windfall created by the housing boom.

But the reality is that many baby boomers do not have sufficient assets or savings to underwrite even a modest retirement. The ABS estimates that around two-thirds of all retirees still depend on government pensions as their primary source of income.

While the dependency on pensions will decline over time, the reality is this generation spent most of their working life in the period before compulsory superannuation.

So baby boomers also expect that younger generations will continue to honour the “intergenerational deal” by underwriting their retirement in the form of pensions, social services and health care.

Political heartburn

As successive governments and policy wonks have been warning for at least a decade, the ageing population presents a major budgetary pressure for Australian governments.

Now, as we face an extended period of slow growth, declining tax revenue and budget deficits, the imperative for reform should be clearer than ever.

The challenging thing for any future government is that the same dynamics that are making pension and super concession reform so difficult will increasingly play out in other policy areas. In everything from health and welfare to public transport and workforce participation, the booming population of older Australians will rightly demand better services to meet their needs.

These are all issues that federal governments were better placed to address over the last two decades, before they became so politically fraught and while we were still enjoying the mining boom.

Now, the politics of ageing will cause growing pain for both sides of politics, shaping their chances of gaining and holding government well into the future.

A more bipartisan, evidence-based approach could enable a sensible policy discussion and the development of more durable policy solutions without so much political heartburn.

Both sides of politics say they are ready to do so, but in light of the current state of Australian politics, it is difficult to be optimistic about this happening any day soon.

Peter Gahan receives research funding from the Australian Research Council, the Commonwealth Department of Employment, the Department of Industry and Science, and Safe Work Australia.